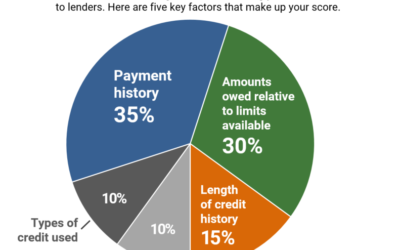

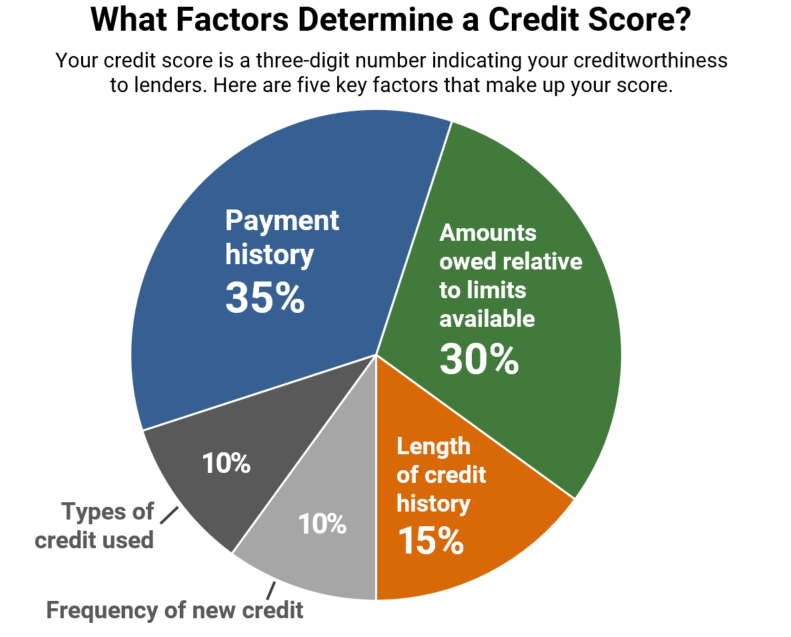

Payment History makes up 35% of your credit score

How you manage your current debt payments counts the most for your credit score. This is where arrear payments will affect your score.

When you cannot pay the full instalment that you signed for, your creditors will list you as a slow payer. This counts for payment arrangements too. If your monthly instalment is R500 and you arrange to pay R300- you will still be listed, even if you pay something.

For good credit management you should be paying more than the minimum due. But many cash strapped South Africans only budget the minimum payment. And when times become more difficult, they default because they can’t keep up.

If your minimum payment is R500 and you budget R750 per month it gives you breathing space during difficult times. The extra R250 you pay monthly will help you squash payment interest quicker. During tough months you can pay R500 and not fall into arrears.

Paying more than the minimum payment will increase your credit score. Paying less than what you owe will drop your score.

Dealing with Arrears

The longer you leave arrears the more it affects your score. That is why the credit bureaus show you how many days you are in arrears when you draw a report.

When you are in arrears your creditors will charge you late payment interest on top of the average 23% you pay. And the longer you leave it, the more it keeps adding up until you owe astronomical amounts.

The best way to deal with this arrear debt is debt restructuring. Using a program like debt counselling will help you to get better interest rates. Our debt experts can arrange rates as low as 9% and in some cases, even 0.

This is bargaining power that the NCR gives to debt counsellors-it’s not a tool you can use in your negotiations. To qualify you must accept the help available and go under the process.

The good news is you will reduce your total outstanding debt. And you benefit now from lower monthly payments. By making consistent payments will improve your score over time. You will also have legal protection to avoid further legal action while you work on the problem.

Conclusion

Your payment history makes up the largest part of your credit score. To fix this you must deal with all arrear debt.

A program like debt counselling will help you deal with all arrear debt without finding extra money in your budget. The lower interest rates will reduce your total debt and monthly debt payments. You get relief without making more debt and once your arrears are paid up, your score will increase.